-2.png?width=500&height=205&name=MIAMI%20HOME%20SEARCH%20(2)-2.png "MIAMI HOME SEARCH (2)-2")

Sales Hit 2-Year High While Buyers Favor Cash

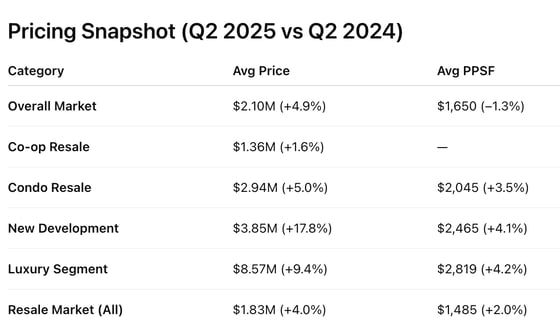

Market ConditionsThe Manhattan real estate market continued its rebound in Q2 2025, with closings reaching their highest level in nearly two years. A total of 3,042 sales closed, marking a 16.6% year-over-year increase and coming in 8.4% abovethe 10-year quarterly average. This was the third consecutive quarter of annual price growth following last year’s declines. Notably, however, about half of the deals were signed before April, ahead of the rollout of the new U.S. tariff policy, which may have helped boost the quarter’s numbers.

Contracts SignedUnlike closed sales which for the most part depicts the past, contracts signed is a leading indicator of the real estate market. Shaking off the uncertainty over tariff policy, Contracts Signed in June 2025 saw a strong surge in newly signed contracts across all property types:

Luxury demand remained the standout. Signed contracts in the $5M–$9.99Mand $10M–$19.99M price bands jumped significantly. For example, condo contracts in the $10M–$19.99M range more than doubled year-over-year. According to the Douglas Elliman Market Report, luxury contract volume (the top 10% of the market) has more than doubled in the past two months alone.

Cash DominatesCash purchases hit a record-high 69.1% of all sales.

|

|

|